Detailed navigation

17. 4. 2017

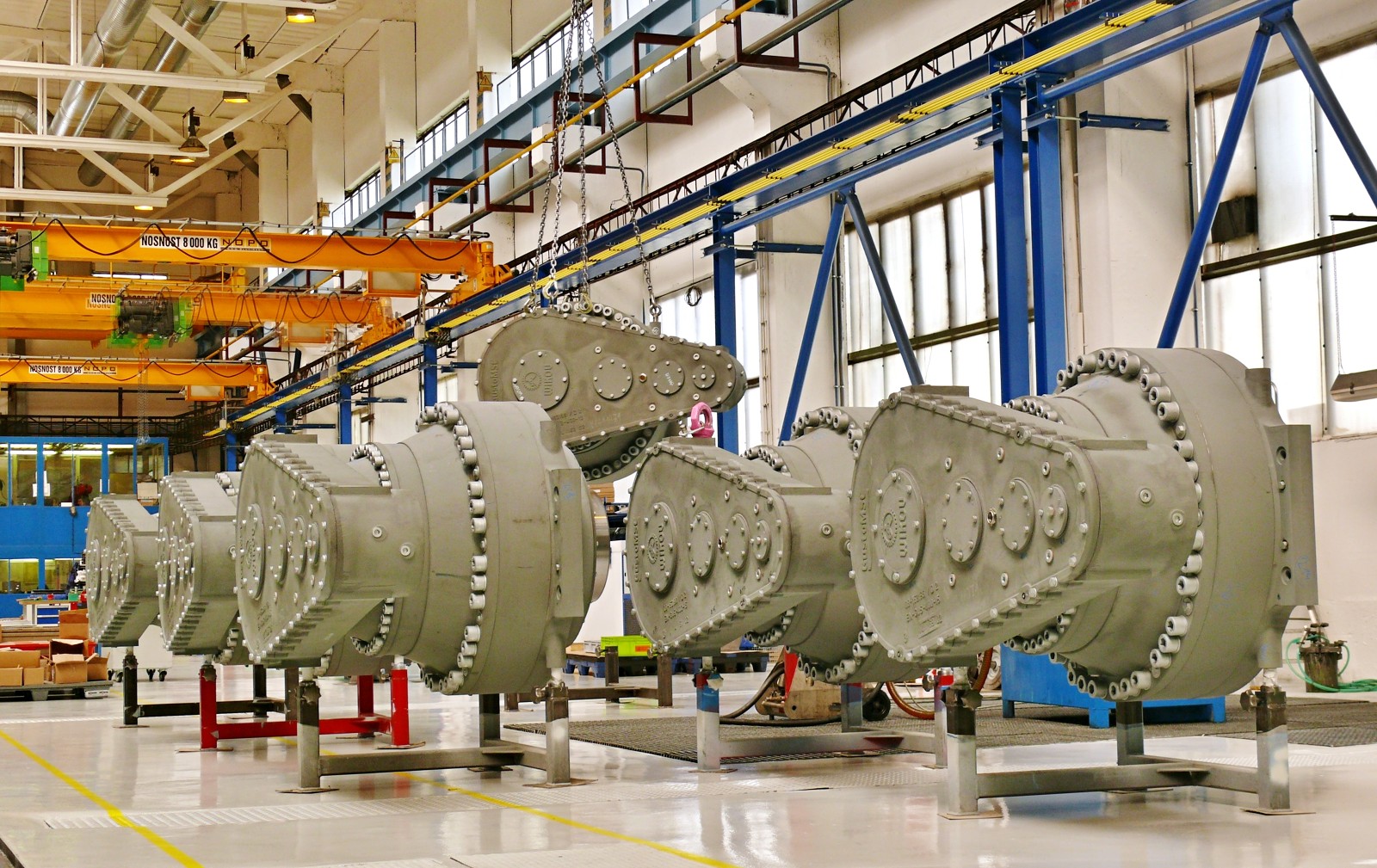

Gearbox manufacturers are focusing on supplying

the aftermarket

Alex Canella, News Editor

The future of the energy industry is a hard one to divine. Whether it’s governmental policies like clean energy grants for wind power and restrictions on fracking or larger, global concerns such as the market price of oil, the industry’s fortunes have always been sensitive to the bigger picture, and that bigger picture has gotten a little blurry. Politically, the United States has become an anything-goes maelstrom, and what the end result will be when the dust settles is anyone’s best guess at the moment. Perhaps more importantly, the industry is also in flux economically. Alternative energy sources are becoming more commercially viable, and while oil isn’t going away anytime soon, just being able to compete is an improvement for alternative energy options that could place those markets in a position to expand. “The market is in the middle of a transformation,” Dipeshwar Singh, global director of strategic marketing at Rexnord, said. “Traditional energy sources are slowly reducing in their share within the energy market, and we are realizing an increase in new forms of energy. We are seeing larger shares of gas, wind, clean coal and solar, and some of the factors that are driving these changes go well beyond the clean, environmental aspect of it. A majority of these new energy sources will continue to be driven by economics. It is becoming increasingly more economical to produce energy through solar, gas or wind, and as it becomes less expensive to produce, the adoption of energy will continue to grow.” In uncertain, changing times, U.S. manufacturers the wind and oil/gas sectors are dealing with very different problems. But before you start breaking out your inner nihilist, there are signs of stability on the horizon.

Oil and Gas: Not out of the Woods Yet

According to the President of Brad Foote Gear Works, Dan Schueller, the oil/gas sector is “all about the price per barrel of oil.” And on that front, the message is still mixed. Some, such as Wikov’s Strategic Marketing Manager, Lukas Steiner, are braced for a few more years of uncertainty for oil, citing continued volatility in the weak oil prices. In the meantime, Wikov is shifting its strategy to focus on low carbon sectors and alternative energy opportunities mostly in the aftermarket and strengthening its position by supplying more gearboxes to those marine applications which are up when oil prices result in significant capex cuts. “We expect volatility in the oil prices while having a price of a barrel still weak,” Steiner said. “We think this will last for some years on. We count on the fact we learned from the history that the oil market takes an awful lot longer to adjust to supply shocks than it does to cyclical demand shocks.” But others like Schueller believe that the industry has finally bottomed out and might be able to expect some stability, though perhaps not a return to the prices of a few years ago. After the industry’s lowpoint of $30 per barrel back in Jan. 2016, the cost of oil managed to claw and scrape its way up to $54/barrel. Seeing the price of oil trend (mostly) positively for a full year is no doubt heartening news for the industry, and improved confidence in the strength of oil could in turn lead to a stronger industry. It could well be the start of a recovery. But even if there’s more cause for celebration than in past years, the oil barrel still has a few hurdles left to leap before anyone can truly start breathing a sigh of relief. Oil’s recent rise can, at least in part, be attributed to the Organization of the Petroleum Exporting Countries (OPEC), which issued a six-month cut on oil production in the hopes of raising prices, and the move has at least inspired confidence in some. “This was the moment not only gear manufacturers but other OEMs were waiting for in hope of later higher capex into a new drilling equipment,” Steiner said. While the price of oil has been going up, the cut’s expiration date is also coming quickly, slated for June 2017, and uncertainty over whether or not the production cut will be extended is already starting to show in the latest market turn for oil, a dip down to $47/barrel. Oil’s greatest hurdle may well be the renegotiation of the production cut, namely getting other heavy hitters like Russia that aren’t a part of OPEC, but are part of the deal, to extend it for another six months. And then there’s the potential for U.S. shale production to pick up and throw a wrench in the works, anyway, which even industry analysts can’t seem to agree on what the potential effect of might be.

While we don’t usually get in the habit of waxing at length about an industry’s political situation, politics are inextricably intertwined with the price of oil.

An oversupplied market naturally driving the cost of oil down leaves artificial cuts in production like OPEC’s, which require a great deal of diplomacy and politicking, as the market’s current hope for stabilizing. Schueller’s optimism, on the other hand, lies in the industry’s ability to adapt to its new circumstances by becoming more streamlined and efficient, which he believes will help the industry stay afloat. “Oil and gas developers have done a good job lowering their costs over those periods so they can be more efficient,” Schueller said. “They can be profitable at oil even though it’s in the upper 40s, lower 50s. I think a few years ago, they would have said the oil price would need to be higher, but everybody’s done a good job cutting costs and trying to become more efficient, so they’re able to be profitable at a lower dollar per oil barrel.”

Coal: Still Facing Headwinds

According to Greg Moreland, global manager of market and product research at Oerlikon Fairfield, the coal industry is still facing its own difficulties related to the low cost of natural gas, a competitor for many of the same wallets as the coal industry. “Despite the recent firming in commodity prices, for equipment manufacturers, the market is still operating at a low point,” Moreland said. “There is a lot of surplus equipment available, and that is impacting replacements for new machinery.” There is some relief on that front, however, as natural gas has climbed in price. Moreland believes that the market’s already weathered the worst, and personally believes that the coal may even see some small growth by the end of the year. “The good news is that these markets have reached a bottom,” Moreland said. “The year over year double digit declines are passed.” According to Dipeshwar Singh, global director of strategic marketing - energy, at Rexnord, there’s also been a shift in the industry as a whole to look at clean coal. “There is currently an enormous focus on clean coal as an identifiable source of new energy,” Singh said. ”Much of the older infrastructure that previously focused on the use of coal will likely be retired. However, there is also the likelihood that a new infrastructure will be developed that is based on the newer, more efficient and cleaner coal technologies.”

Wind: The Big Crunch

The wind market is looking at better prospects. The wind market is looking at better prospects. Late in 2015, Congress passed a 5-year production tax credit for wind power producers that phases down over that time period. This has provided the U.S. wind industry with the longest outlook in its history, adding stability where there used to be little. And the industry’s focus on cutting down the cost of wind energy and becoming economically competitive with oil and gas is already bearing fruit. According to the AWEA, the fourth quarter was the second strongest ever for wind power installations. But according to Martin Sychrovsky, Wikov’s marketing director, the industry isn’t likely to stop there. “There will continue [to be] a huge pressure to reduce costs and further reduction in prices of the turbines,” Sychrovsky said. For the wind market, this is healthy. There’s no telling if or when the government might bless the industry with more tax credits, and after years of governmental hemming and hawing over funding nascent wind energy efforts, making commercial sense is going to be just as important for the industry to expand as any environmental argument. For manufacturers, however, it’s just one of many factors that are leading people to expect a big crunch in the industry moving forward. As prices are driven down in an effort to compete with oil, the ability to build and sell in bulk will become an important factor in staying competitive in the industry. “Nowadays the market suffers from excessive overcapacity,” Steiner said. “And for us, a smaller player, [there] is less space in there.” “Increasingly, this business will pay off only for the big players which are able to achieve economies of scale,” Sychrovsky said. For U.S. gear manufacturers in particular, the problem is compounded by the strength of the dollar. When faced with a competitive global market in which competitors are actively trying to drive down prices, it’s doubly difficult to match foreign prices with the added weight of a strong U.S. dollar. Though the wind market is doing well, smaller players may have difficulty competing with larger companies, particularly foreign ones. In the meantime, Schueller’s best advice to anyone still looking to make gears for the front-end wind market is to look at reducing material costs and increasing productivity. “The two major buttons to push are how do you reduce your material costs and how do you make your factory more productive to produce that gear?” Schueller said. It’s standard advice, and perhaps easier said than done for small manufacturers, but it’s also proven. Brad Foote has focused intently on reducing costs and increasing efficiencies over the past several years. According the Schueller, “Brad Foote is focusing more on the aftermarket where lead-time and responsiveness are important.”

A Single Solution

Despite wildly different woes between each industry, everyone seems to have come to the same solution on how to stay profitable in uncertain times: the aftermarket. For the wind industry, the aftermarket looks like the most lucrative opportunity in the market today. While smaller gear manufacturers may have trouble finding business for brand new gearboxes, the aftermarket is still wide open for their services. “The boom occurs in the aftermarket,” Sychrovsky said. “Conventional wind turbine gearbox life is 6-7 years. Even the first Chinese offshore parks look around after the first exchanges. There is a very promising future in repairs and replacements business.” With the wind turbine industry being overtaken by the big players, the aftermarket is a logical place to migrate to. With a turnaround that short, old wind turbines will always be hungry for new gearboxes. According to Schueller, however, wind turbine gearboxes have seen a wealth of improvements in the past decade. From new designs to sensors that can detect potential mechanical problems early, Schueller believes that U.S. gear manufacturers have come far in improving the design of wind turbine gearboxes. Those advances have made gearboxes stronger and longer-lasting. “It would be hard to point to one particular thing that would say ‘hey, this is what has really caused it to get better,’”

Schueller said. “As with most times, it’s a combination; combination of better designs, combination of better gear manufacturing by the gear manufacturers, better repair, better monitoring and better early detection of potential problems. Where I think the first gearboxes ran into failure, I think now the early detection is catching problems before a major failure occurs.” One might think that the existence of better, more durable gearboxes would put a damper on the aftermarket, but Wikov and Brad Foote are expecting that the improved gearboxes will actually be a selling point in their favor. At the same time as old, less sophisticated gearboxes are in need of replacement, this new wave of gearboxes are hitting the aftermarket along with assurances such as Wikov’s that the gearbox won’t have to be replaced again: “We are confident about extended lifetime of our solution so with the installation of Wikov gearbox, the customer will not have to replace it until the end of the wind turbine lifetime,” Sychrovsky said. It stands to reason that these higher quality gearboxes would be snapped up. And according to Schueller, improved gearboxes will increase demand for aftermarket services such as gear regrinding, as well. Schueller has found that some of the more recent gearboxes don’t always need gears fully replaced, but instead just require some regrinding to touch them up. This results in cheaper repair costs and a win-win for both Brad Foote and gearbox users. For industries like oil and coal, the basic hope is that once the markets pick back up, coal and oil miners alike will be hungry for more equipment after skimping on replacement parts and utilizing other cost-cutting methods during leaner years. “Our optimism lies in the hope that sooner or later some of the existing equipment will reach the end of its lifetime and will have to be replaced,” Steiner said. “This will be the moment for us to say it was a good decision to stay in this market segment and not to leave it for other segments Wikov serves.” “During this last cycle, many mines were not only delaying new equipment purchases, but they were also cutting back on maintenance,” Moreland said. “Spare parts were being cannibalized from existing used machinery. When the markets turn upward, there is going to be increased demand for not only replacement parts, but also for new equipment. There is going to be a ‘bullwhip’ effect that will challenge manufacturers. Those who will benefit will be the ones with strong supply chains which can be ramped up to meet higher volumes.” Flexibility could be important going forward. If markets continue to remain low, it will be important to maintain low operating costs to stay buoyant, but if conditions improve, a wave of demand brought on by mining companies with more spending money won’t wait for businesses to reestablish themselves. But until the day those conditions improve and the energy industry sorts itself out, there’s always the aftermarket.